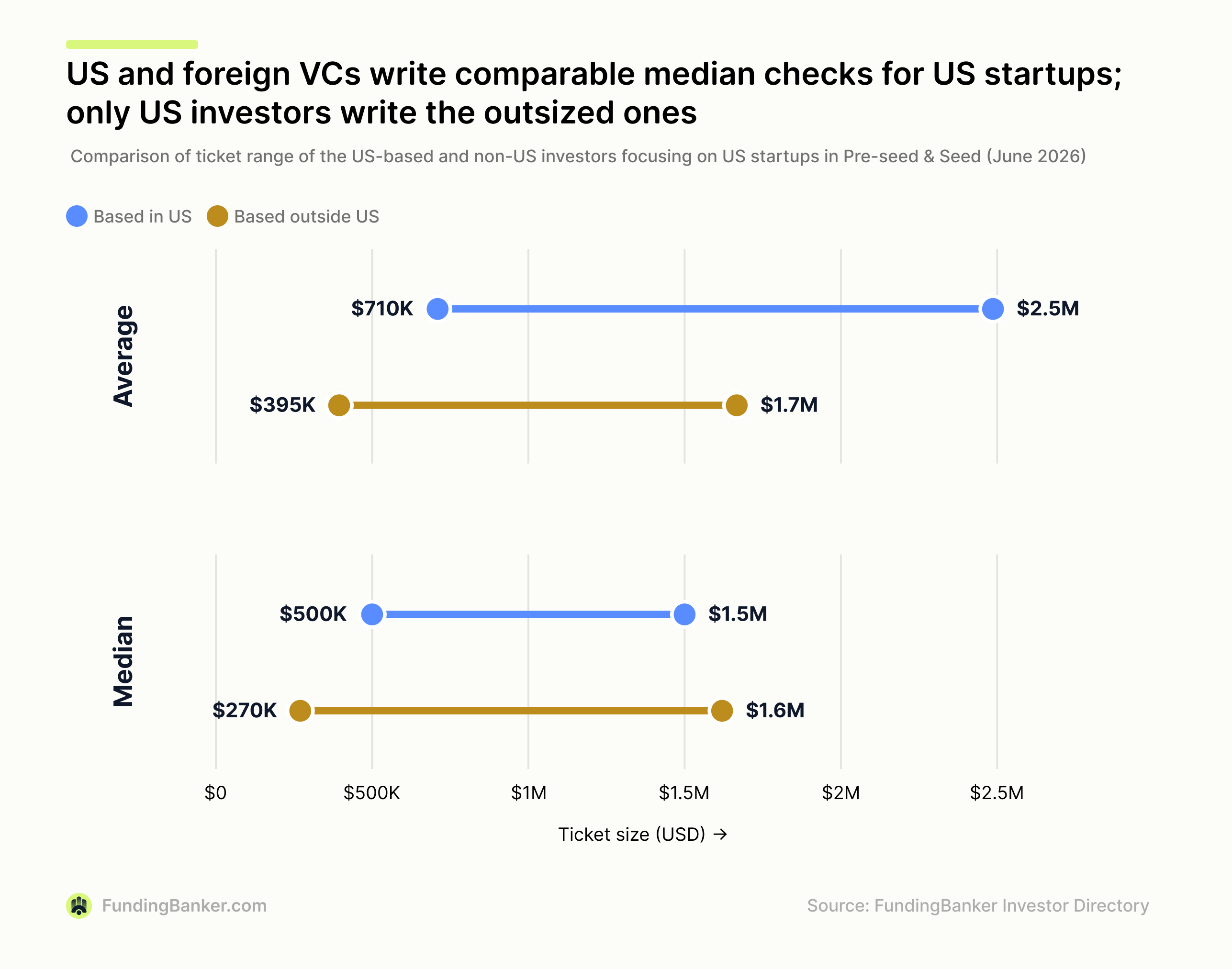

We ran an analysis against our investor directory on the 2nd of June, 2026, comparing the US-based and Non-US based investors that were:

- Supporting US-based startups

- Focus exclusively on Pre-Seed and/or Seed

- Have a public ticket size

We used the average and median of the lower and upper bounds of the ticket sizes provided by the investors.

Here are the findings, as visible on the chart:

| Median | Average | |||

|---|---|---|---|---|

| Low | High | Low | High | |

| US-Based | $500k | $1.5m | $710k | $2.5m |

| Non-US-based | $270k | $1.6m | $395k | $1.7m |

Comparing the medians, US-based investors have a ~2x larger lower bound, while the upper bound is comparable between the two groups.

Comparing the averages, the image is very different. Having the median, we know that the standard US-based investor is not writing much larger check sizes than their foreign counterparts, but there are American outliers, writing checks large enough to skew the average to the right, by a considerable margin.

What does this mean?

I interpret this as a signal that foreign investors are more active in smaller rounds, and if participating in larger rounds, acquire smaller shares of the startups. This discrepancy, in my opinion, will lead to further consolidation of American ownership in startups that are very capital-intensive, such as Aerospace, Quantum, Compute, etc.

Non-US investors, however, have a meaningfully lower bound, which puts them in a good position to take ownership of promising startups in their earliest days, which in the long run, can yield a higher ROI.